Navigating the world of estate law often feels like trying to read a map in a thunderstorm, especially when the federal government starts moving the landmarks. For the last few years, everyone in the legal and financial world was bracing for the "2026 Sunset," a moment when estate tax exemptions were scheduled to drop significantly. However, with the passage of the One Big Beautiful Bill Act in mid-2025, the landscape has shifted again. Now, the federal estate tax exemption sits at a staggering $15 million per individual.

At Sutton Law Office, we know that when you see headlines about multi-million dollar tax caps, it can feel a bit disconnected from daily life here in South Central Indiana. You might be wondering if these massive numbers have any impact on your family’s farm, your small business, or the home you’ve worked decades to pay off. We believe in providing compassionate and practical solutions that cut through the noise, helping you understand exactly what applies to you and what is simply "big city" chatter.

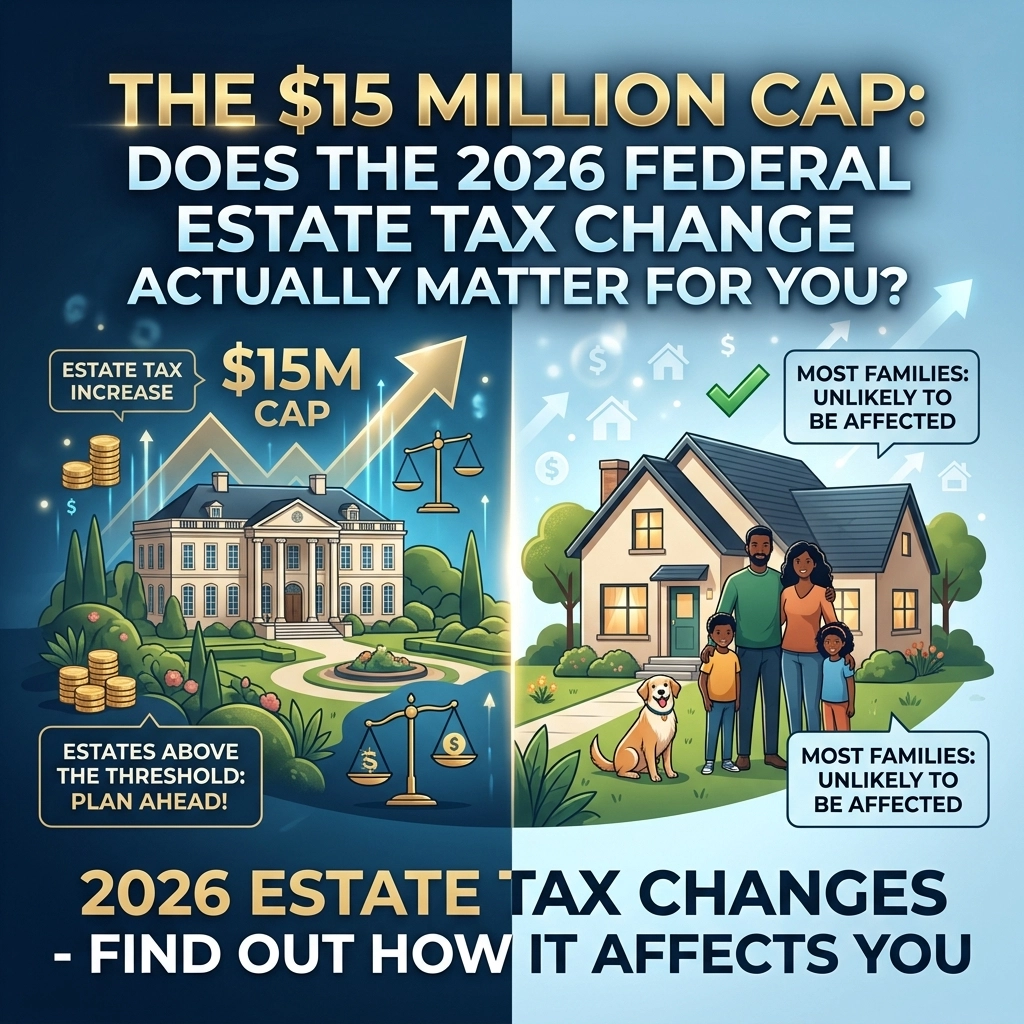

The New Reality of the $15 Million Exemption

To understand where we are now, we have to look at where we almost were. For several years, the tax law stated that the high exemption amounts we enjoyed would "sunset" or expire on January 1, 2026. If that had happened, the exemption would have been cut roughly in half, falling to about $7 million per person. While that is still a lot of money, it was low enough to start catching many more family farms and successful small business owners in the tax net.

With the new legislation passed in July 2025, that "cliff" was avoided. The federal exemption is now set at $15 million per individual, or a combined $30 million for a married couple. Even better for long-term planning, this amount is now permanent and indexed annually for inflation. This provides a level of certainty we haven’t seen in the estate planning world for a very long time.

So, let’s answer the big question right away: Does this matter for the average family in South Central Indiana? For the vast majority of our neighbors, the answer is no: at least not in the way of owing a massive tax bill to the IRS. Most estates in our community do not reach the $15 million mark. However, that doesn’t mean the news is irrelevant. Understanding why you don't have to worry about this tax can provide immense peace of mind, allowing you to focus on the things that actually do matter, like avoiding probate and protecting your kids' inheritance.

Why "Tax-Free" Doesn't Mean "Hassle-Free"

It is easy to hear that your estate is "under the limit" and assume that you don't need an estate plan. This is a common misconception that we encounter frequently. While the federal government might not be taking a 40% cut of your hard-earned assets, there are plenty of other "taxes" on your time, sanity, and family harmony if you haven't prepared.

When we talk about estate planning at Sutton Law Office, we focus on protection and clarity. Even if you aren't worried about the $15 million cap, you should be thinking about:

- Probate Costs: Indiana probate can be a slow and public process. Even a "small" estate can lose thousands of dollars in court costs, filing fees, and administrative expenses if it isn't structured correctly.

- Family Dynamics: Without a clear plan, your heirs are left to guess your intentions. This is often where the most significant "cost" occurs: the breakdown of family relationships during a stressful time.

- Long-Term Care: For many Hoosiers, the real threat to an inheritance isn't the federal estate tax; it's the cost of a nursing home. Planning for Medicaid eligibility is far more pressing for most families than worrying about a $15 million tax threshold.

We strive to offer clear and tailored guidance that addresses these local realities. You can learn more about how we handle these specific Indiana challenges at https://estates.jsuttonlaw.com.

The High-Stakes Side: Who Actually Needs to Worry?

While the $15 million cap covers most people, there is a segment of our community that needs to take this very seriously. South Central Indiana is home to some incredible multi-generational farms and thriving local industries. If you own several hundred acres of quality land, equipment, and a home, or if you’ve built a company from the ground up, you might be surprised at how quickly your valuation approaches that $15 million mark: especially when you factor in life insurance payouts and retirement accounts.

For those who do cross that threshold, the federal estate tax is no joke. The tax rate for amounts over the exemption is a flat 40%. That is a massive chunk of a family legacy that could have been preserved with the right tools. We often work with high-net-worth individuals to implement ethical and creative strategies like Irrevocable Life Insurance Trusts (ILITs) or Family Limited Partnerships.

The IRS has confirmed that "lifetime gifts" made under current exemptions will not be "clawed back" if future legislation ever lowers the limit again. This means that if you are in that high-wealth bracket, now is the time to act. Using your $15 million exemption today through gifting can lock in those savings for your children and grandchildren.

Gifting: A Strategy for Everyone

One part of the federal tax law that does impact almost everyone is the annual gifting exclusion. For 2026, this limit is $19,000 per recipient. This means you can give $19,000 to your son, $19,000 to your daughter, and $19,000 to each of your grandkids every single year without it ever touching your $15 million lifetime limit. If you are married, you and your spouse can combine this to give $38,000 per person, per year.

This is a compassionate and practical way to see your family enjoy their inheritance while you are still around to witness it. Whether it's helping a grandchild with a down payment on a house or funding a 529 college savings plan, annual gifting is a powerful tool. It reduces the size of your estate (which helps with Medicaid planning later) and puts money where it’s needed most right now.

Looking Beyond the Numbers

At the end of the day, estate planning isn't about the IRS. It’s about the people you love. Whether the federal limit is $5 million or $50 million, the goals of a good estate plan remain the same:

- Ensuring your spouse is cared for without having to navigate complex court systems.

- Naming guardians for minor children so that a judge doesn't have to make that choice for you.

- Protecting assets from potential creditors or future ex-spouses of your beneficiaries.

- Making your wishes known regarding end-of-life care and medical decisions.

We believe that every family deserves the same level of protection and professional care, regardless of their net worth. Our team at Sutton Law Office is dedicated to being your trusted advocate, ensuring that your transition of wealth is as smooth and stress-free as possible.

Your Next Steps

The headlines about the $15 million cap are a great reminder to check in on your own plan. If it’s been more than three years since you last looked at your will or trust, or if you’ve had a major life change like a birth, death, or marriage in the family, it is time for a review.

The laws have changed, the exemptions have shifted, and your life has likely changed too. Don't face these emotionally and legally complex decisions alone. We are here to provide the stability and guidance you need to protect what you've built.

Whether you are looking for a basic will or a complex trust to manage a large family estate, we invite you to connect with us. We offer solution-oriented and efficient legal services designed to give you peace of mind. You can visit our main site at https://jsuttonlaw.com to see our full range of services or call our office to schedule a consultation.

Let's make sure your plan is based on your reality, not just the latest headlines from Washington. Contact Sutton Law Office today, and let’s build a legacy that lasts.

Leave a Reply